Warren Buffett Steps Down After Six Decades, Leaving a Trillion-Dollar Empire and a Canon of Enduring Investment Wisdom

As Berkshire Hathaway’s leadership passes to Greg Abel, Buffett’s letters resurface as a roadmap of discipline, restraint, and moral clarity in finance

Warren Buffett is preparing to step away from the leadership of Berkshire Hathaway, bringing to a close more than six decades at the helm of one of the most influential companies in modern financial history.

At ninety-five, Buffett is handing control to Greg Abel, marking the end of an era on Wall Street defined not only by extraordinary returns, but by an unusually coherent philosophy of capitalism.

Buffett transformed Berkshire Hathaway from a struggling New England textile company into a global conglomerate valued at approximately one point one trillion dollars.

The group now spans railroads, insurance, energy, and infrastructure, while holding around three hundred fifty billion dollars in cash and short-term bonds and roughly two hundred eighty-three billion dollars in equities.

Few investors in history have combined such scale with such longevity.

As Buffett prepares to withdraw from day-to-day leadership, attention has returned to the annual letters he wrote to shareholders over sixty years.

Those letters were not technical manuals.

They were essays, rich in metaphor and blunt honesty, laying out how capital should be allocated and how power should be exercised.

Buffett compared poor acquisitions to biblical mistakes, warned against paying for businesses with overvalued shares, and openly admitted errors that cost shareholders dearly.

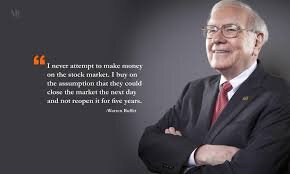

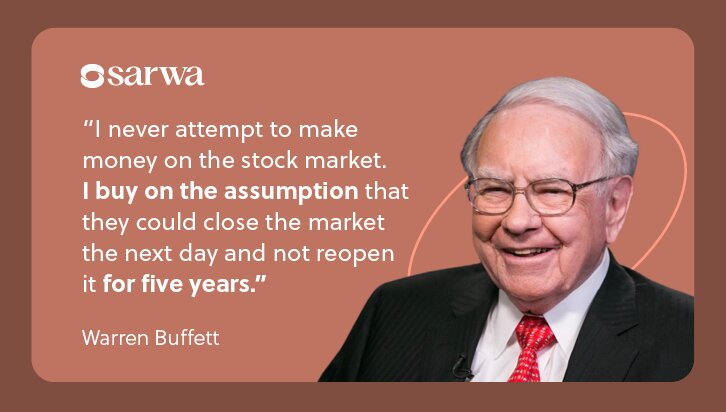

He repeatedly emphasized the difficulty and importance of buying entire, high-quality businesses at sensible prices.

He explained his dual strategy of owning minority stakes in exceptional public companies while seeking full ownership of others, using humor to make the point that flexibility multiplies opportunity.

He cautioned chief executives against listening too eagerly to deal-hungry advisers, likening such encouragement to advice that solves no real problem.

Buffett’s warnings about risk proved prescient.

He described financial derivatives as weapons of mass destruction years before the global financial crisis, later arguing that excessive leverage and opaque interdependence among institutions had made catastrophe inevitable.

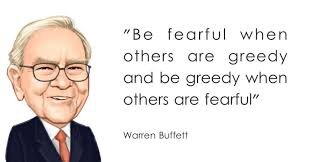

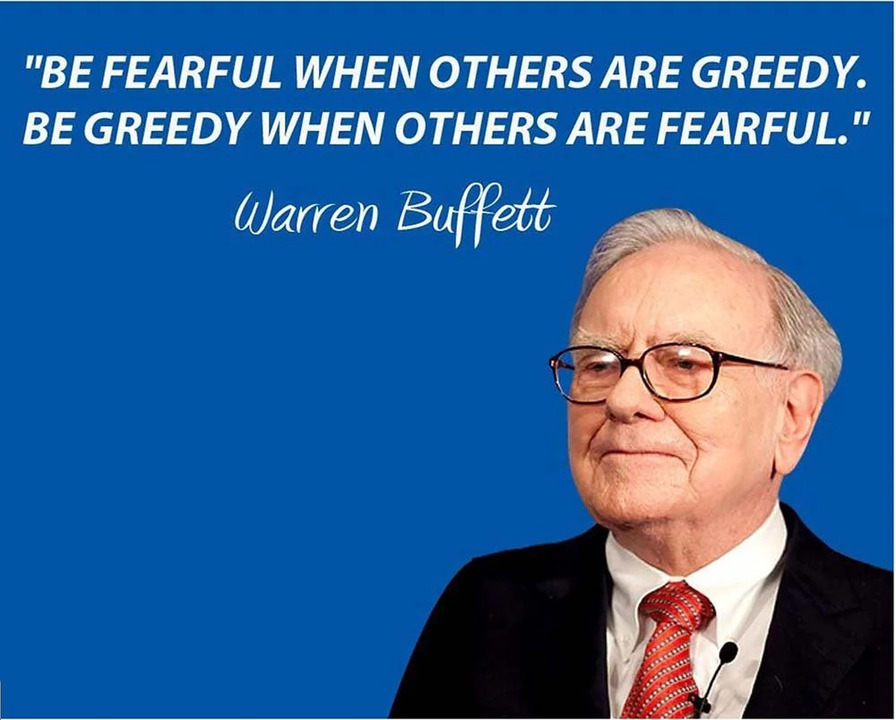

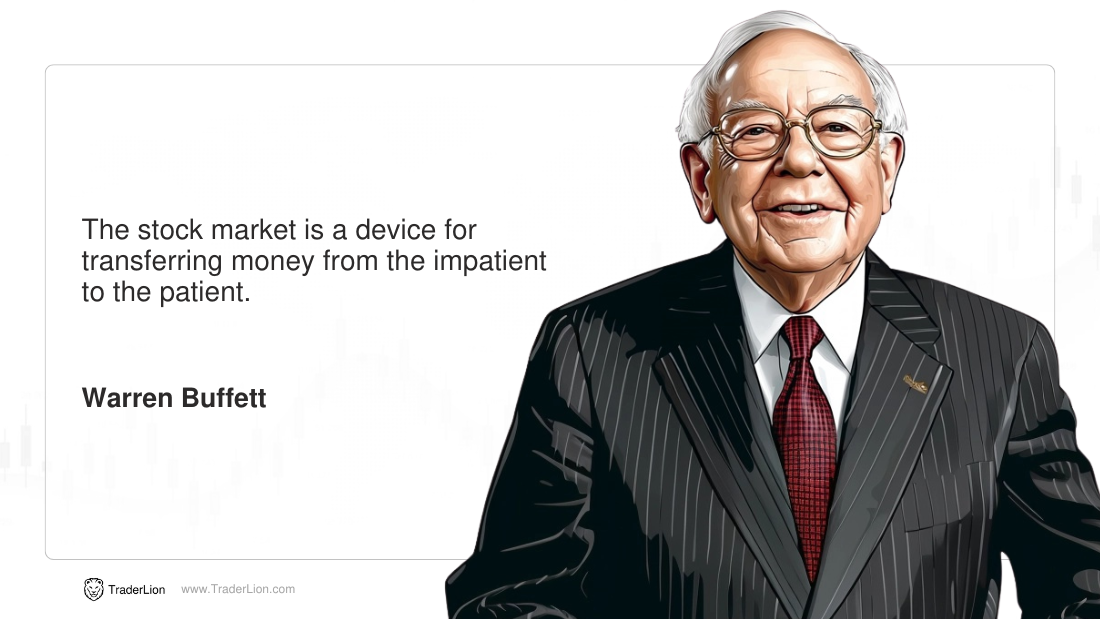

At the same time, he insisted that downturns create opportunity, urging investors to act boldly when fear dominates markets.

Beyond strategy, Buffett cultivated a moral reputation rare in high finance.

He was widely admired for fair dealing, patience, and restraint, traits that earned Berkshire unusual trust and flexibility.

As he steps back, he has made clear that he will no longer write the annual letters or dominate the company’s shareholder meetings, choosing silence after a lifetime of explanation.

What remains is a body of work that continues to shape how investors think about value, risk, and responsibility.

Buffett leaves behind not just a company, but a standard against which modern capitalism is still measured.

At ninety-five, Buffett is handing control to Greg Abel, marking the end of an era on Wall Street defined not only by extraordinary returns, but by an unusually coherent philosophy of capitalism.

Buffett transformed Berkshire Hathaway from a struggling New England textile company into a global conglomerate valued at approximately one point one trillion dollars.

The group now spans railroads, insurance, energy, and infrastructure, while holding around three hundred fifty billion dollars in cash and short-term bonds and roughly two hundred eighty-three billion dollars in equities.

Few investors in history have combined such scale with such longevity.

As Buffett prepares to withdraw from day-to-day leadership, attention has returned to the annual letters he wrote to shareholders over sixty years.

Those letters were not technical manuals.

They were essays, rich in metaphor and blunt honesty, laying out how capital should be allocated and how power should be exercised.

Buffett compared poor acquisitions to biblical mistakes, warned against paying for businesses with overvalued shares, and openly admitted errors that cost shareholders dearly.

He repeatedly emphasized the difficulty and importance of buying entire, high-quality businesses at sensible prices.

He explained his dual strategy of owning minority stakes in exceptional public companies while seeking full ownership of others, using humor to make the point that flexibility multiplies opportunity.

He cautioned chief executives against listening too eagerly to deal-hungry advisers, likening such encouragement to advice that solves no real problem.

Buffett’s warnings about risk proved prescient.

He described financial derivatives as weapons of mass destruction years before the global financial crisis, later arguing that excessive leverage and opaque interdependence among institutions had made catastrophe inevitable.

At the same time, he insisted that downturns create opportunity, urging investors to act boldly when fear dominates markets.

Beyond strategy, Buffett cultivated a moral reputation rare in high finance.

He was widely admired for fair dealing, patience, and restraint, traits that earned Berkshire unusual trust and flexibility.

As he steps back, he has made clear that he will no longer write the annual letters or dominate the company’s shareholder meetings, choosing silence after a lifetime of explanation.

What remains is a body of work that continues to shape how investors think about value, risk, and responsibility.

Buffett leaves behind not just a company, but a standard against which modern capitalism is still measured.

Translation:

Translated by AI